Introduction

Poland’s ancillary services market has reached an inflection point. The total value of FCR, aFRR, mFRR, and RR reserve auctions now exceeds PLN 2 billion annually, and the market continues to grow. Meanwhile, average aFRR reserve rates in Poland stand at approximately PLN 180/MW/h — four times higher than Germany (PLN 45–55/MW/h) and more than double the Netherlands (PLN 80–90/MW/h).

These figures are striking. But there’s a catch: simply owning a battery energy storage system doesn’t automatically grant access to these revenues. Entering the balancing market requires navigating a certification process, building the right IT infrastructure, meeting NC RfG technical requirements, and obtaining Balancing Service Provider status.

For many investors, this process remains opaque. This article provides a practical guide to Poland’s balancing market from a BESS project perspective: what the market is, how it works following the 2024 reform, what the formal and technical requirements are, and what you need to do to get in the game.

What Is the Balancing Market and Why Does It Matter for BESS?

The balancing market is a technical market operated by PSE (Polskie Sieci Elektroenergetyczne), Poland’s transmission system operator (TSO). Its primary function is to balance electricity supply and demand in real time, maintaining grid frequency at 50 Hz.

Here’s how it works in practice: trading companies buy and sell energy on the wholesale market in advance — typically the day before delivery or earlier. But forecasts are never perfect. Wind blows stronger or weaker than predicted, clouds block the sun, a factory ramps up production, a power plant trips. These gaps between plan and reality must be balanced by PSE, which activates units capable of rapidly increasing or reducing output.

This is where energy storage enters the picture. BESS is an ideal candidate for ancillary services for several reasons:

Response speed. Storage responds in milliseconds, not minutes. A gas plant needs several minutes to change output; a coal plant needs even longer. Storage adjusts almost instantaneously.

Bidirectionality. BESS can both inject energy into the grid (when there’s a shortage) and absorb it (when there’s excess). This makes it a symmetric resource — particularly valuable to PSE.

Dispatch precision. If PSE needs exactly 5 MW, storage delivers exactly 5 MW. Not 4.8 MW, not 5.3 MW. Gas and coal turbines simply can’t match this accuracy.

Zero fuel cost at standby. A conventional power plant must run at minimum load to remain ready to respond — generating fuel costs and emissions. Storage waits “for free.”

This is why ancillary services are considered one of the primary revenue streams for BESS projects in Poland, alongside capacity market payments and price arbitrage. In financial models for utility-scale storage, ancillary service revenues often account for 40–60% of total income in the early years of operation.

Why Now? A Window of Opportunity for Early Movers

The current environment of high prices and limited competition is temporary. Ancillary service rates are elevated because the supply of flexible resources remains constrained — Poland’s system is still dominated by conventional and pumped-storage plants, with battery storage only just entering the market.

Over the next two years, more than 1 GW of new energy storage and at least 4 GW of solar and wind capacity capable of providing ancillary services will connect to the national grid. As supply increases, prices will fall — that’s basic market dynamics.

What does this mean for investors? Those who enter first will benefit most. Early movers gain access to the highest rates, build operational experience, and establish relationships with aggregators or PSE before the market becomes saturated. Delayed entry means competing in a more crowded and demanding environment.

A Respect Energy report states plainly: “The early development phase is characterised by high rates and low competition, favouring above-average margins. Generators that prepare their assets technically and operationally now will gain both financial and strategic advantage.”

The Balancing Market Reform of 14 June 2024 — What Changed?

On 14 June 2024, the second phase of Poland’s balancing market reform came into force, fundamentally changing the rules of the game. This wasn’t a cosmetic adjustment — it was a comprehensive overhaul that opens the market to new technologies and participants.

Settlement Period Shortened to 15 Minutes

Previously, balancing energy was settled on an hourly basis. Now there are 96 settlement periods per day instead of 24. The balancing energy price and imbalance price are determined separately for each 15-minute interval.

What does this mean in practice? Greater granularity equals more precise price signals — but also higher requirements for resource flexibility and IT systems. Your EMS must report data and respond in 15-minute cycles, not hourly ones.

Market Opening for Smaller Players

Entities with capacity from 0.2 MW are now formally eligible to participate in the balancing market, down from the previous 1 MW threshold. The reform also introduced the possibility for smaller participants to combine into larger groups participating jointly — known as aggregation.

In theory, this opens the market to smaller storage systems. In practice — as we’ll discuss shortly — 1 MW remains the effective minimum due to bid volume requirements.

New Entity Structure: BSP and BRP

The reform introduced a clear distinction between two roles:

Balancing Service Provider (DUB in Polish) — the entity that actually provides ancillary services to PSE. This is who controls the assets (storage, power plant, DSR), submits bids to the balancing market, and executes operator instructions.

Balance Responsible Party (POB in Polish) — the entity responsible for commercial balancing, i.e., for differences between scheduled and actual generation/consumption.

The key change: you can now be a BSP without being a BRP. A storage owner can provide ancillary services while transferring balance responsibility to another party — such as a trading company or aggregator. This significantly simplifies market entry for asset owners.

New Unit Categories and Services

The reform introduces new object categories — Balancing Units (JB) and Scheduling Units (JG) — and harmonises the ancillary services catalogue with European standards:

- FCR (Frequency Containment Reserve) — primary frequency response

- aFRR (automatic Frequency Restoration Reserve) — secondary frequency response

- mFRR (manual Frequency Restoration Reserve) — tertiary frequency response

- RR (Replacement Reserve) — replacement reserve

The technical requirements, rates, and qualification procedures for each of these services will be covered in a follow-up article.

Poland Joins the PICASSO Platform — A Step Change in July 2025

On 11 July 2025, PSE operationally joined the European aFRR balancing energy exchange platform — PICASSO (Platform for the International Coordination of Automated frequency restoration and Stable System Operation). This represents a fundamental shift.

What Is PICASSO?

PICASSO is a pan-European platform where transmission system operators buy and sell energy needed to balance their grids in real time. Rather than activating only domestic resources, PSE can now access the cheapest available bids from across Europe — and conversely, Polish providers can sell balancing energy to other countries.

What Does This Mean for Polish Energy Storage?

Access to foreign markets. If your storage is certified as a BSP and provides aFRR services, your bids can be activated not only by PSE but also by operators from the Czech Republic, Germany, Austria, and other countries connected to PICASSO.

Increased competition. This works both ways — Polish providers now compete with foreign ones. If a Czech plant offers a lower price, PSE may activate it instead of a Polish storage system.

Potential price pressure. In the long term, European integration may lead to price convergence between countries. Currently, Polish aFRR rates are significantly higher than the European average — this gap will likely narrow over time.

Greater short-term volatility. Following PICASSO integration, significant price spikes have emerged. For example, on 11 July 2025 the balancing market price was deeply negative, while on 15 July it was extremely high. This is the new reality that market participants must prepare for.

Joining PICASSO ended the era of a closed, domestic system and opened the aFRR market to genuine international competition. It’s a fundamental change for anyone planning to earn from ancillary services.

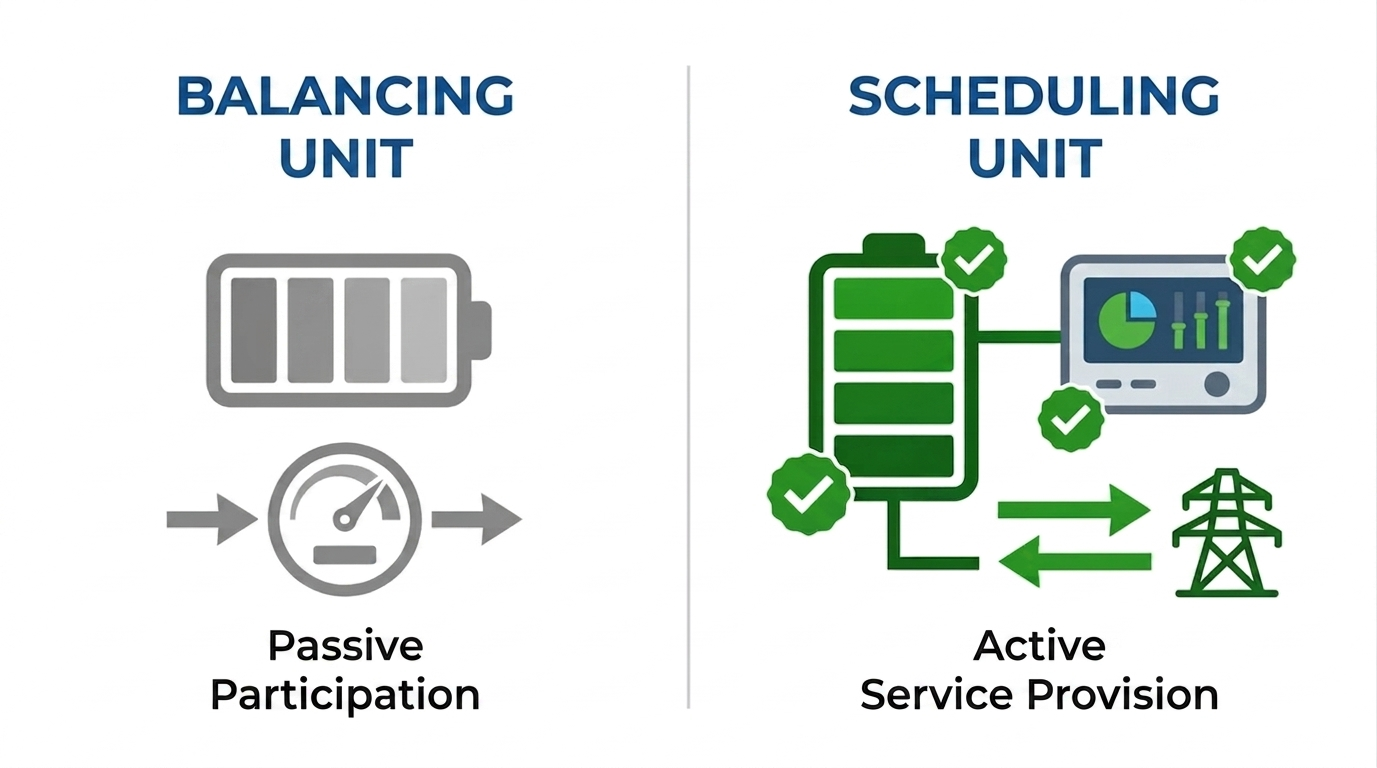

Balancing Units vs Scheduling Units — A Critical Distinction

This is where many BESS project developers get confused. A question I hear frequently: “Once I’m connected to the grid, can I automatically provide ancillary services?” The answer is no. And the distinction is fundamental.

Balancing Unit (JB) — Passive Participation

A Balancing Unit is a collection of delivery points for which commercial balancing is conducted. Every grid-connected asset — whether energy storage, a wind farm, or a factory — automatically becomes part of its BRP’s (Balance Responsible Party’s) Balancing Unit.

This is passive participation: you settle imbalances, meaning the difference between what you scheduled (declared in your dispatch programme) and what actually entered or left the grid. If you produced more than declared, you sell the surplus at the balancing market price. If less, you buy the shortfall.

Scheduling Unit (JG) — Active Service Provision

A Scheduling Unit is something quite different. It’s a collection of resources used to provide ancillary services. In other words, you create a Scheduling Unit only when you want to actively participate in the balancing market — submitting bids for FCR, aFRR, or mFRR and executing PSE instructions.

Creating a Scheduling Unit is a deliberate choice, not an automatic status. It comes with specific obligations:

- You must have a SOWE system for PSE communication

- You must submit dispatch programmes for the unit

- You must submit balancing bids

- You must meet qualification criteria for the relevant reserve type

- You must be capable of executing operator instructions within the required timeframe

Scheduling Unit Types for Energy Storage

For energy storage, there are two main Scheduling Unit types:

JGM1 — storage scheduling unit with full dispatch. PSE can issue instructions across the full capacity range. If you have a 10 MW storage system, PSE can instruct you to charge at full power or discharge at full power, at any time when you’re qualified for the service.

JGM2 — storage scheduling unit with limited dispatch. Here you have more control — you decide how much capacity to offer in each period. PSE can only dispatch what you’ve offered in your balancing bid.

Which type to choose? It depends on your business strategy. JGM1 offers greater revenue potential from system services (PSE has full access to your capacity) but less flexibility. JGM2 enables revenue stacking — you can offer part of your capacity to the balancing market while using the rest for price arbitrage or other purposes.

The Activity Marker (ZAK) — Who Decides?

Each Scheduling Unit has an assigned activity marker (ZAK) that defines the scope of PSE dispatch. This is an important parameter affecting your operational flexibility.

ZAK=1 — full dispatch. PSE can issue instructions across the unit’s full capacity range. This is mandatory for large thermal plants subject to central dispatch (JWCD).

ZAK=2 — limited dispatch. PSE dispatches only within the scope of the bid submitted by the BSP. This is the typical choice for energy storage and RES — you decide how much capacity to make available to PSE in each period.

ZAK=3 — for aggregated units. Used for Scheduling Units comprising multiple small resources combined through an aggregator.

Who chooses the ZAK? For energy storage, the BSP — meaning you or your aggregator — selects the ZAK in the qualification application. PSE doesn’t impose a marker for storage systems. It’s your business decision.

Practical example: You have a 10 MW storage system and select ZAK=2. In the morning, spot market prices look attractive for arbitrage, so you submit a balancing bid for only 5 MW. You use the remaining 5 MW for arbitrage. By afternoon the situation changes — you submit a bid for 8 MW. You retain full flexibility.

Minimum Capacity — Why You Effectively Need 1 MW

According to the Balancing Terms and Conditions, the minimum capacity for a Scheduling Unit is 0.2 MW. But that’s the absolute technical minimum. In practice, to actively participate in the balancing market, you need at least 1 MW.

Why 1 MW When Regulations Say 0.2 MW?

This stems from minimum bid volume requirements for FCR, aFRR, and mFRR markets. The minimum size of a single balancing bid is 1 MW. You cannot submit a bid for 300 kW or 500 kW — the system won’t accept it.

So theoretically you can create a Scheduling Unit with a 200 kW storage system, but you won’t be able to submit any bids. It’s like having a driving licence but no car.

Maximum Scheduling Unit Capacity

There’s also an upper limit — the maximum capacity for a single Scheduling Unit is 50 MW. If you have a larger project, you’ll need to split it across multiple units.

The Solution for Smaller Storage — Aggregation

What if your storage system is smaller than 1 MW? You can’t enter the market independently. But there’s a solution — aggregation. You can combine several smaller resources through an aggregator, which creates an aggregated Scheduling Unit (JGA).

Requirement: Resources must be connected to the same 110 kV network node (or to a network managed by the same DSO for medium and low voltage resources). You can’t aggregate a storage system in Warsaw with one in Kraków.

The aggregator combines your asset with others in its portfolio, creating a virtual unit exceeding 1 MW that can submit bids to the balancing market. You receive a share of revenues proportional to your contribution.

Technical Requirements — NC RfG, Certificates, and Standards

Before you start thinking about BSP certification, you need to ensure your storage system meets the basic technical requirements for grid connection and operation. This is the foundational layer — without it, you won’t get anywhere.

The NC RfG Network Code — Mandatory Certification

Since 1 May 2022, every generating device (including energy storage operating as a source) must hold a certificate of compliance with Commission Regulation (EU) 2016/631, known as the NC RfG (Network Code on Requirements for Generators).

The certificate confirms that the equipment meets technical requirements regarding:

- Operating frequency and voltage ranges

- Fault ride-through capability (FRT)

- Active and reactive power regulation capability

- Response to operator signals

No certificate = no connection. The DSO will refuse to sign a connection agreement for an installation without a valid NC RfG certificate. This isn’t optional — it’s mandatory.

The PTPiREE List — The “White List” of Devices

The Polish Association of Electricity Transmission and Distribution (PTPiREE) maintains an official registry of devices holding NC RfG certificates recognised in Poland. The list is updated every two weeks and currently contains over 1,800 entries.

Before purchasing equipment: Check whether your chosen inverter/PCS and storage model appears on the PTPiREE list. Visit ptpiree.pl, find the “Network Codes” section, and search for the model. If it’s not there — don’t buy it, or ensure the manufacturer has a concrete timeline for obtaining certification.

Watch the firmware versions: The list specifies the minimum required software version. If you have older firmware, you’ll need to update before connection.

Technical Standards for Energy Storage

Beyond NC RfG, energy storage systems should comply with various technical standards:

IEC 62619 — safety requirements for lithium-ion batteries in industrial applications

IEC 62933 — electrical energy storage systems (a series covering terminology, parameters, and safety)

IEC 62477-1 — safety requirements for power converters (applicable to PCS)

EN 50549 — requirements for generating units connected to distribution networks (often required as an NC RfG supplement)

What This Means for Investors

Before purchasing equipment: Require confirmation from suppliers that devices have NC RfG certification and appear on the PTPiREE list. Request certificate numbers and verify them independently.

In supplier contracts: Include a condition that delivered equipment must hold valid certificates enabling connection in Poland. Specify consequences for non-compliance.

Don’t buy “bargains” without certificates: Cheaper equipment without certification may prove worthless if the DSO refuses connection.

Communication with PSE — The LFC, SOWE, and WIRE Systems

Now we come to what is perhaps the most technically challenging topic: communication with PSE. This isn’t simply a matter of purchasing the right equipment — it involves system integration, testing, connection certification, and infrastructure maintenance.

PSE has three main systems for data exchange with balancing market participants. You need to understand how they differ and which is required for what.

The LFC System (Load Frequency Control) — For aFRR

This is the automatic frequency and power regulation system. It’s the heart of aFRR services — automatic frequency restoration reserve.

How does it work? The central LFC node at PSE monitors grid frequency and calculates the required regulation power. It then sends control signals every second to Scheduling Units connected via external LFC nodes. These signals instruct: “increase output by X MW” or “reduce output by Y MW.”

Your storage system must automatically execute this instruction — without human intervention, in real time. The EMS receives the signal from LFC and passes it to the PCS controller, which adjusts storage output. The entire cycle must complete within seconds.

Requirements: Dedicated LFC node (hardware + link to PSE), communication latency below 1 second, tests confirming correct response to signals.

The SOWE System — For All Ancillary Services

The Operational Cooperation System with Balancing Service Providers. This is the platform for exchanging business documents between BSPs and PSE.

Through SOWE you submit:

- Dispatch programmes for Scheduling Units (how much energy you plan to produce/consume in each period)

- Balancing bids (how much capacity you’re offering and at what price)

- Activation confirmations (PSE informs you that your bid has been activated)

SOWE is required for every BSP providing aFRR or mFRR services. Without a SOWE connection, you cannot submit balancing bids.

The WIRE System — Market Information

A system for exchanging capacity market data and unit parameters. Used primarily for reporting and information exchange rather than real-time operations.

Practical Implications

To provide aFRR services, you need both SOWE (for bid submission) and LFC (for automatic regulation). For mFRR, SOWE alone is sufficient — regulation is manual, not automatic.

Building the communication infrastructure represents a significant investment in hardware, software, and integration. But there’s an alternative — you can use an aggregator’s infrastructure.

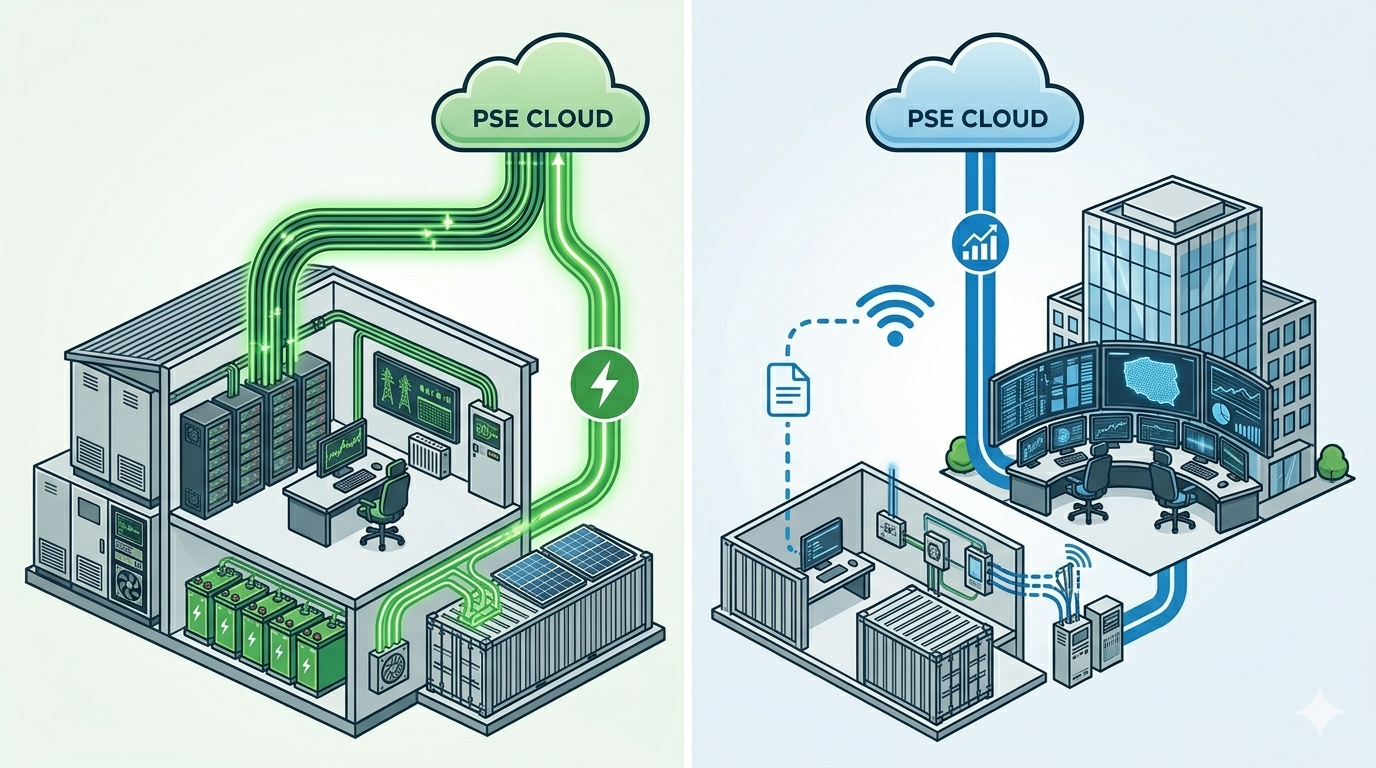

Local Node vs Remote Node — A Concrete Architectural Decision

Since we’re discussing LFC and SOWE nodes, I need to clarify something that often causes confusion. “Node” sounds abstract, but this is very specific equipment in a very specific location.

Local Node — Full Control, Higher Costs

A local node is infrastructure physically installed at your energy storage facility, in a technical building or control container. It comprises:

- Communication server — receives signals from PSE, processes them, and passes them to the EMS

- Industrial firewall — cybersecurity protection (required under NIS2)

- Router with dedicated PSE link — typically VPN over internet or a leased line

- Backup power system — PSE communication cannot be interrupted during grid outages

Costs: Building a local node runs approximately PLN 200,000–400,000 for hardware and integration alone. Add to this PSE connection certification costs plus ongoing maintenance — links, licences, technical support, and updates.

When it makes sense: A local node makes sense when you have a large project (say 20 MW or more) and plan to be a standalone BSP. All infrastructure is on your premises, giving you full control but also full responsibility for maintenance.

Remote Node — Lower Costs, Less Control

A remote node provides the same functionality but located elsewhere — typically at an aggregator’s operations centre or a company providing operational services.

How does it work? The aggregator has its own LFC node connected to PSE. It receives control signals for all resources in its portfolio, then passes the appropriate instructions to individual storage systems via its own connection (usually encrypted internet).

From PSE’s perspective, the signal goes to the aggregator’s node. From your storage system’s perspective, the instruction comes from the aggregator, not directly from PSE.

Costs: You bear no infrastructure construction costs. You pay the aggregator a commission on revenues — typically 20–30% at market rates.

When it makes sense: For smaller projects, for investors without IT/OT capabilities, for those wanting rapid market entry without building their own infrastructure.

Comparison

| Aspect | Local Node | Remote Node |

| Upfront cost | PLN 200,000–400,000 | None (aggregator’s responsibility) |

| Ongoing costs | Maintenance, links, support | 20–30% revenue commission |

| Control | Full | Limited |

| IT responsibility | Yours | Aggregator’s |

| Implementation time | Longer (construction, certification) | Shorter (aggregator integration) |

| Viability threshold | Large projects (>15–20 MW) | Smaller projects |

The BSP Certification Process — Stages and Pitfalls

What does the journey look like from “I have an energy storage system” to “I’m providing ancillary services”? The BSP certification process comprises four main stages.

Stage 1: Application Submission

You submit an application to PSE at kwalifikacja@pse.pl. The application must include:

- Full technical specification of the asset

- Capacity parameters (maximum capacity, minimum capacity, ramp rate)

- Connection information (connection point, voltage, DSO)

- Control and communication system documentation

- NC RfG certificates and other required documents

Document templates are available on the PSE website. Everything must be signed with a qualified electronic signature.

Stage 2: DSO Verification

If your storage system is connected to the distribution network (most are), the application goes through the local DSO (ENEA, ENERGA, PGE, TAURON, or Stoen). The DSO verifies:

- Technical data and consistency with the connection agreement

- Communication capability (appropriate protocols and links)

- Compliance with IRiESD requirements

Stage 3: PSE Confirmation

PSE analyses the application, verifies that technical criteria for the relevant service type are met, and issues qualification confirmation. This is when you officially become a Balancing Service Provider.

This stage may require verification tests — PSE can demand demonstration that your storage system actually responds as declared.

Stage 4: Contract Execution

Finally, you enter into an electricity transmission services agreement with PSE (if you don’t already have one) plus an annex or separate agreement covering ancillary services provision.

How Long Does It Take?

PSE’s official timeline allows 3–4 months for the entire process. But that’s theory. In practice — especially for first-of-a-kind energy storage projects — it may take longer.

Common Pitfalls

IT systems integration. Communication between your storage EMS and PSE platforms (SOWE, LFC) isn’t “plug and play.” It requires protocol adaptation, testing, and debugging. Every BESS supplier has slightly different solutions, and PSE has its own requirements. Allow at least 2–3 months for IT integration alone.

Pre-qualification tests. Before receiving full qualification, you must pass verification tests. That the storage system actually responds within the declared time. That it can deliver the declared capacity. That communication works reliably. That the LFC system responds to signals in under one second. One failed test means a repeat several weeks later.

Cybersecurity requirements. The NIS2 Directive introduces new obligations for energy sector entities. PSE will verify whether communication systems meet security requirements. If you lack a cybersecurity policy, incident response procedures, and network security measures — you may have a problem.

Inexperience on both sides. Poland’s utility-scale energy storage market is only just developing. PSE doesn’t yet have dozens of BESS certification cases under its belt. Contractors are learning too. This means the process may be more iterative than documentation suggests.

Aggregator vs Independent Certification — Which Path to Choose?

This question comes up in virtually every conversation about the balancing market. Let’s first clarify the terminology.

BSP and Aggregator — Not the Same Thing

Balancing Service Provider (DUB) is a formal market role defined in regulations. A BSP provides ancillary services to PSE. This can be the owner of a single large storage system, or equally a company aggregating multiple smaller resources.

Aggregator is a business model — an aggregator combines multiple smaller resources into a single portfolio and represents them collectively in the market. An aggregator is a BSP, but not every BSP is an aggregator.

If you have a 20 MW storage system and go through certification yourself — you’re a BSP (independent). If a company combines your 5 MW storage system with other storage systems and represents them together to PSE — that company is an aggregator (and also a BSP).

When Does an Aggregator Make Sense?

Your storage system is smaller than 1 MW. You can’t submit a balancing bid independently — you need aggregation with other resources.

You don’t want to build IT infrastructure. The aggregator already has SOWE and LFC nodes, optimisation systems, and an operations team. You just connect your storage system to their platform.

You lack energy trading expertise. Submitting optimal bids on the balancing market is an art. The aggregator does this daily for dozens of assets — they have experience, algorithms, and historical data.

You want rapid market entry. Independent certification and infrastructure construction takes at least 6–12 months. With an aggregator, you can start providing services 2–3 months after signing a contract.

How Much Does an Aggregator Cost?

Typical aggregator commission is 20–30% of ancillary service revenues. This may seem substantial, but remember:

- You avoid node construction costs (PLN 200,000–400,000)

- You avoid ongoing infrastructure maintenance costs

- You don’t need to hire energy trading specialists

- The aggregator may optimise better than you could independently (scale effects, algorithms)

For smaller projects (up to 10–15 MW), the aggregator model often works out better even after accounting for commission.

When to Go Independent?

You have a large project (>20 MW). At this scale, fixed infrastructure costs spread across more megawatts, and commission savings make a real difference.

You have a project portfolio. If you’re planning to build 5 storage systems at 10 MW each, it makes more sense to invest in your own BSP infrastructure and handle them all yourself.

You have internal capabilities. If your company already has energy trading experience, an IT/OT team, and understands the market — you can do it yourself.

You want full control. Some investors simply don’t want to depend on an external party for a key revenue stream.

Market Status in 2026 — Where Are We?

In January 2026, Poland’s first licence for electricity storage was issued. It went to the BESS facility at Nowe Czarnowo with 24 MW capacity and 56 MWh storage, owned by Israeli company Energix. This marked a breakthrough moment — but it also shows how early we are in this market’s development.

BSP Certification — The Process Is Taking Longer Than Expected

The Nowe Czarnowo storage system obtained its licence and completed integration with Axpo’s VPP STELLAR platform. However, at the time of writing (April 2026), the balancing market qualification process is still ongoing. Axpo, which took over commercial and technical-regulatory operation of the storage system, declared back in autumn 2025 that it would begin providing ancillary services for energy storage from Q1 2026.

That deadline wasn’t met. Q1 2026 has passed, and no utility-scale battery storage system in Poland is yet providing full ancillary services as a BSP.

This shouldn’t surprise anyone familiar with first-of-a-kind implementation realities. The qualification process involves technical tests, IT system integration with PSE platforms (SOWE, LFC), DSO verification, and final operator approval. Each stage can encounter unforeseen problems — especially when dealing with the country’s first projects of this type.

What Does This Mean for Investors?

Pioneer risk is real. No ready templates, learning on the fly, extended certification processes. Those planning BESS projects with assumptions of rapid balancing market entry should build in realistic time buffers — not 3–4 months as official documents suggest, but 6–12 months.

First-mover opportunity still exists. Despite delays, aFRR rates remain high. Whoever completes certification first will capture the early-entry premium — before the market becomes saturated.

Rates will decline. Current aFRR rates of approximately PLN 180/MW/h reflect limited supply. As new storage and RES enter the market, prices will converge toward Western European levels (PLN 45–90/MW/h). The question isn’t whether, but when — and who will capitalise on the current window.

Project Pipeline

Much more is on the horizon. Several large storage systems are planned for commissioning in 2026–2027:

- BESS Jedwabno — 150 MW / 300 MWh, R.Power, optimisation by Axpo, connection by end of 2028 (capacity contract from 2029)

- BESS EDP Renewables — 60 MW / 241 MWh, Wielkopolskie voivodeship, operational start planned for 2027

- TAURON projects — BESS Przewóz, BESS Dąbie, BESS Proszówek, BESS Kuźnia Raciborska

Estimates suggest that 7–8 GW of battery energy storage may be commissioned in Poland in the coming years. The project pipeline — from capacity auctions to connection applications — varies in different estimates from 4 GW to as much as 40 GW.

Summary: What You Need to Know

The balancing market is a technical market where PSE buys flexibility to keep the system in balance. Following the June 2024 reform, it’s formally open to energy storage from 0.2 MW — but the practical entry threshold is 1 MW due to minimum bid volume requirements.

Poland is one of Europe’s most attractive ancillary services markets — aFRR rates here are four times higher than in Germany. But this window is closing. Those who enter first will benefit most.

A Scheduling Unit isn’t an automatic status upon grid connection. It’s a deliberate choice to actively participate in the balancing market, bringing specific obligations — having SOWE/LFC systems, submitting dispatch programmes, and placing bids.

The activity marker (ZAK) is chosen by the BSP — meaning you or your aggregator. You can select ZAK=2 and retain flexibility over how much capacity you offer to the balancing market versus other uses.

NC RfG technical requirements are mandatory. Without a certificate on the PTPiREE list, you cannot connect your storage system to the grid — and therefore cannot even begin thinking about BSP certification.

PSE communication requires LFC systems (for aFRR) and SOWE (for all services). These system nodes must be built and maintained by the BSP — either you (PLN 200,000–400,000 plus ongoing costs) or your aggregator (20–30% commission).

BSP certification officially takes 3–4 months but may take longer for early projects. Common pitfalls include IT integration, pre-qualification tests, and cybersecurity requirements.

Poland’s PICASSO integration (July 2025) opens the market to European competition. Polish providers gain access to foreign markets but also compete with foreign entities.

We’re at the beginning. Poland’s first electricity storage licence was issued in January 2026, and the first BSPs with storage systems are starting up in Q1 2026. This is a moment worth being part of — but you need to be aware of pioneer risk.

FAQ — Frequently Asked Questions

Can I enter the balancing market with a 500 kW storage system?

Not independently — the minimum balancing bid size is 1 MW. But you can join an aggregator that will combine your storage system with other assets into a portfolio exceeding 1 MW. Requirement: assets must be in the same network area (same 110 kV node or DSO).

How long does BSP certification take?

Officially 3–4 months from complete application submission. In practice — for first-of-a-kind energy storage projects — it may take 6–9 months, allowing for IT integration time, tests, and potential corrections.

Aggregator or independent certification — which should I choose?

It depends on scale and capabilities. For projects up to 10–15 MW, an aggregator typically makes more sense — you avoid infrastructure costs (PLN 200,000–400,000), and the 20–30% commission is the price for rapid market entry and professional optimisation. For projects above 20 MW or portfolios of multiple storage systems — consider independent certification.

What IT systems are required to provide ancillary services?

It depends on the service type. For mFRR, SOWE is sufficient (document exchange with PSE). For aFRR, you also need LFC (real-time automatic regulation, signals every second). The storage EMS must integrate with these platforms.

Do I need an NC RfG certificate to become a BSP?

Yes, indirectly. The NC RfG certificate is required for grid connection of your storage system. Without connection, you cannot provide ancillary services. So it’s a prerequisite — first NC RfG and connection, then BSP certification.

Will rates fall after Poland joined PICASSO?

In the long term — probably yes. European integration leads to price convergence between countries. Currently, Polish aFRR rates are significantly higher than Western European levels, so there’s room to fall. But the process will be gradual — we’re talking years, not months.

Sources

- URE — “The second phase of the Balancing Market reform enters into force today” (June 2024): https://www.ure.gov.pl/pl/urzad/informacje-ogolne/aktualnosci/12002

- Gramwzielone.pl — “The best time to earn from ancillary services” (November 2025): https://www.gramwzielone.pl/magazynowanie-energii/20342656

- Ecoekonomia.pl — “Energy storage and RES are taking over the balancing market” (November 2025): https://ecoekonomia.pl/2025/11/24/magazyny-energii-i-oze-przejmuja-rynek-bilansujacy/

- PSE — “PSE operationally joined the PICASSO platform” (July 2025): https://www.pse.pl/-/pse-operacyjnie-dolaczyly-do-platformy-picasso

- Bankier.pl — “Balancing market reform and changes to energy settlement” (June 2024): https://www.bankier.pl/wiadomosc/Reforma-rynku-bilansujacego-i-zmiana-sposobu-rozliczen-za-energie-staly-sie-faktem-8765132.html

- Prawo.pl — “Energy market: The second phase of the Balancing Market reform enters into force” (June 2024): https://www.prawo.pl/biznes/drugi-etap-reformy-rynku-bilansujacego-zalozenia,527496.html

- WNP.pl — “A new market era is coming for RES and energy storage” (October 2025): https://www.wnp.pl/energia/nadchodzi-nowa-era-rynkowa-dla-oze-i-magazynow-energii-warto-byc-pierwszym,1000520.html

- Gramwzielone.pl — “Poland’s first electricity storage licence issued” (January 2026): https://www.gramwzielone.pl/magazynowanie-energii/20346881

- PSE — “RfG” (NC RfG requirements): https://www.pse.pl/kodeksy/rfg

- PTPiREE — “Certificate Registry”: https://ptpiree.pl/en/actions-network-codes/list-of-certificates/

- PTPiREE — “Terms and Procedures for Certificate Use” (version 1.3, March 2024): https://ptpiree.pl/en/actions-network-codes/conditions-and-procedures/

- naszrynekenergii.pl — “PICASSO aFRR — European balancing energy platform” (November 2025): https://naszrynekenergii.pl/picasso-afrr-europejska-platforma-energii-bilansujacej/

Listen to the Podcast

More on The Balancing Market and Certification Process for BESS projects Episode 14 of the GreenEdge – Best in BESS podcast

Related articles:

Financing Energy Storage in Poland: How to Finance a BESS Project in 2026

NIS2 and Cybersecurity in BESS Projects: New Obligations for Investors in Poland

BESS + PV: Why Hybrid Projects are the Future of Poland’s Renewable Energy Market