Introduction

In December 2025, Poland’s National Fund for Environmental Protection and Water Management (NFOŚiGW) announced the results of its energy storage subsidy competition. A total of 183 projects with combined capacity of nearly 4 GW and 14.5 GWh received recommendations, backed by a budget exceeding PLN 4 billion (ESS News). This marks a breakthrough moment for Poland’s energy storage market.

However, the subsidy recommendation is just the beginning. Between NFOŚiGW’s decision and project commissioning lies the process of securing bank financing – and this stage proves far more challenging for many investors than anticipated.

Financial institutions approach BESS projects with caution. Unlike solar or wind farms, which have established positions in bank portfolios, energy storage remains a relatively new asset class. This translates to higher documentation requirements, more conservative financial model assumptions, and the need to present a convincing commercial structure.

This article presents key aspects of BESS project financing in Poland: the financial institutions’ perspective, available optimizer cooperation models, public subsidy challenges, and practical guidance for preparing a project for bank discussions.

The Financial Institutions’ Perspective

Energy Storage as a New Asset Class

Financing a solar farm relies on a relatively simple model: energy production depends on irradiation, and revenues – on energy prices or PPA terms. Both variables are reasonably predictable over multi-year horizons, and banks have developed standardized approaches to evaluating such projects.

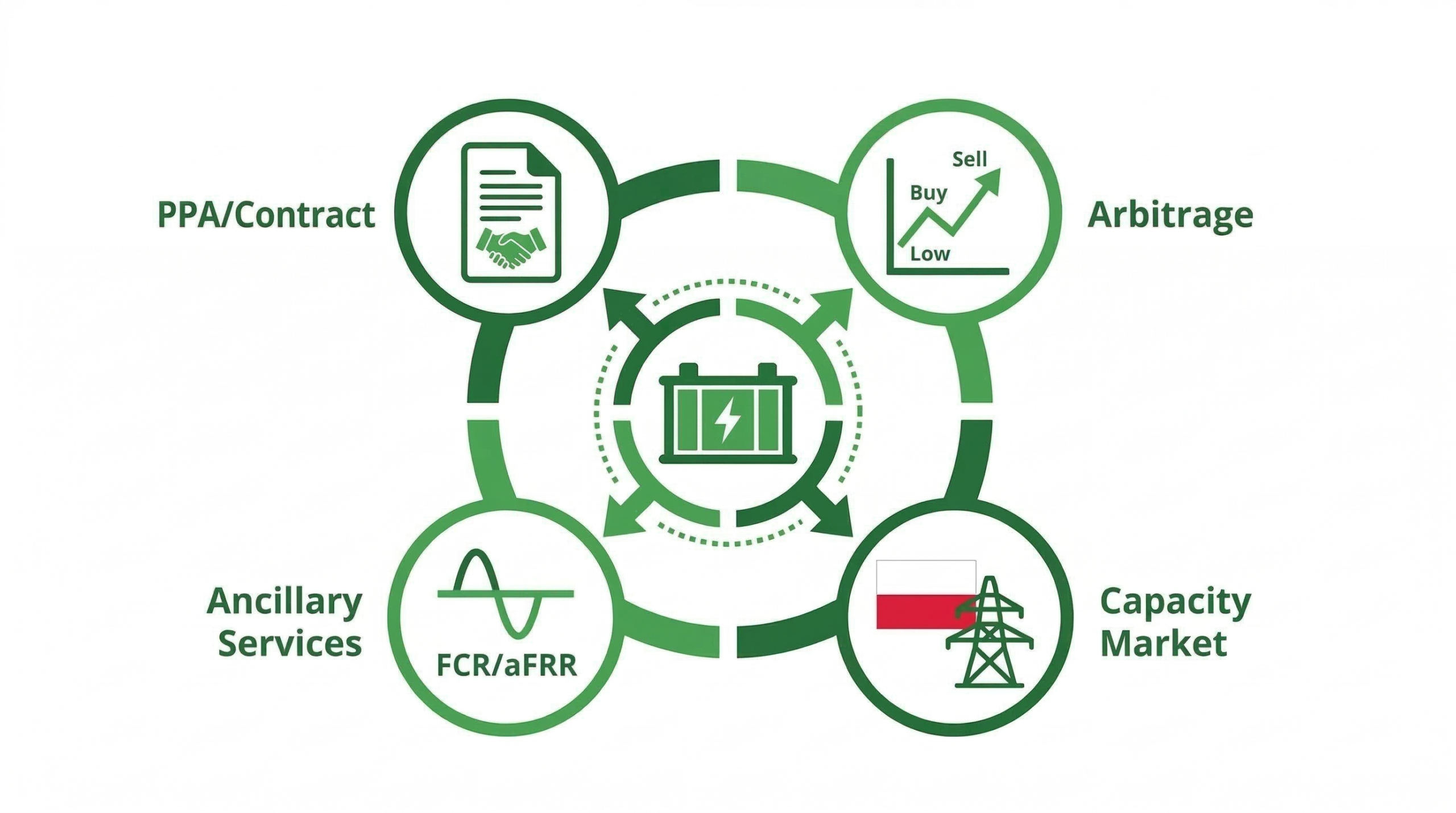

Energy storage operates on different logic. It doesn’t produce energy – it manages it. Revenues come from the difference between purchase and sale prices (arbitrage), ancillary services, and capacity market participation. Each of these streams has a different risk and predictability profile.

For financial institutions, this means evaluating a significantly more complex business model. Notably, this situation resembles the period several years ago when PV financing was challenging due to the banking sector’s lack of experience with this asset class. Over time, banks developed standards and PV became a routine credit product. A similar evolution awaits the BESS sector – though it currently remains at an early stage of this path.

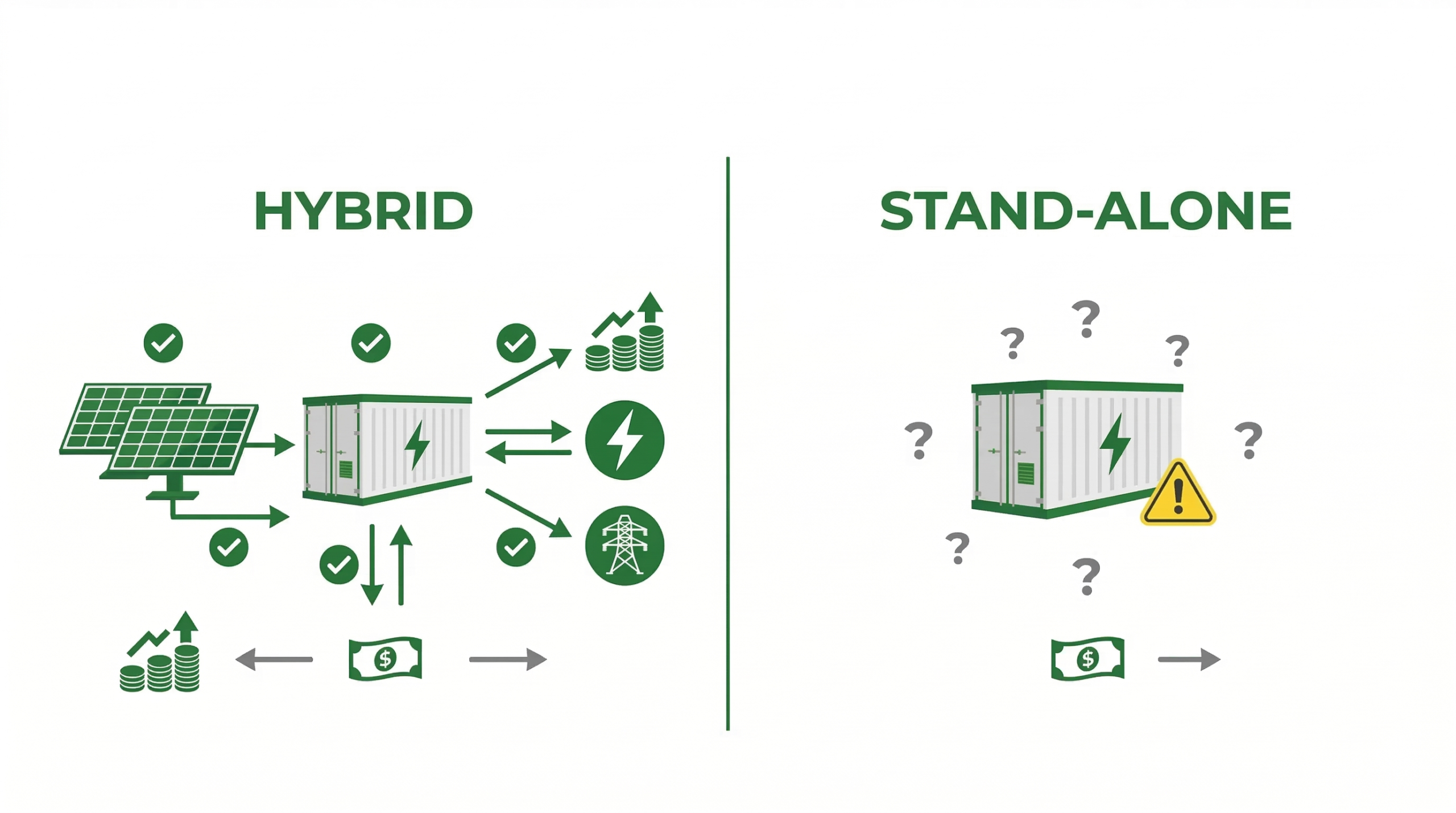

Hybrid vs. Stand-alone Projects

A key factor affecting BESS project bankability is its configuration – standalone storage or installation integrated with a generation source (hybrid).

Hybrid projects – energy storage paired with PV or wind farms – attract significantly more interest from financial institutions. The reasons include:

- Revenue diversification – the project generates revenues from both energy production and storage optimization

- Curtailment risk mitigation – storage absorbs energy surpluses that would otherwise be lost from a standalone PV farm

- Understandable business model – the bank sees a traditional RES project with an additional value-enhancing component

Data from the Polish market confirms the growing scale of curtailment. According to Forum Energii, in the first nine months of 2025, PSE curtailed RES production by over 1.1 TWh – significantly more than the 731 GWh for all of 2024. For hybrid projects, energy storage provides natural protection against these losses.

Stand-alone storage requires a different approach to financing structuring. Without a generation component, the entire business model relies on energy management and service provision. This generates higher requirements for revenue security and operator experience.

DSCR and Credit Requirements

The fundamental measure of a project’s ability to service debt is the DSCR (Debt Service Coverage Ratio) – the ratio of annual cash flows available for debt service to annual principal and interest payments.

According to Norton Rose Fulbright data from 2024, typical DSCR requirements for projects with long-term contracts were as follows:

| Project Type | Typical Minimum DSCR (P50, 2024) |

| PV Farm with PPA | 1.25 – 1.30 |

| Wind Farm with PPA | 1.30 – 1.40 |

| BESS | ~2.0 |

It should be noted that the above data comes from early 2024. As the BESS market matures and banks gain experience with initial projects, we observe gradual relaxation of requirements. Nevertheless, the difference remains significant – energy storage still requires substantially higher DSCR than traditional RES projects, reflecting higher perceived risk associated with revenue volatility.

Higher DSCR requirements mean the project must generate significantly greater cash surplus, which translates to lower leverage or the need to secure more stable revenue streams – hence the role of the capacity market and tolling agreements.

Capacity Market as Business Plan Foundation

In current market conditions, a capacity market contract constitutes the primary revenue-stabilizing element for large energy storage projects in Poland. Multi-year agreements (15-17 years) with guaranteed payments for capacity availability address financial institutions’ key need – cash flow predictability.

However, the auction for delivery year 2030 brought a significant parameter change. The de-rating factor for energy storage dropped from 60% to just 13%. In practice, this means a project with 100 MW physical capacity receives payment for only 13 MW of obligated capacity.

According to Energy Storage News (ess-news.com), in the 2030 auction, BESS projects won contracts for approximately 685 MW of obligated capacity – significantly less than 2.5 GW in the previous year. With low de-rating, however, the actual physical capacity to be built amounts to approximately 5.1 GW.

The de-rating decline has fundamental consequences for financing structuring. Projects without capacity market contracts must rely more heavily on other revenue sources – primarily optimizer agreements.

Optimizer Cooperation Models

An optimizer is the entity responsible for managing energy storage on markets – making charging and discharging decisions, participating in the balancing market, and providing ancillary services. This requires trading infrastructure, optimization algorithms, licenses, and a qualified team.

Most energy storage investors lack such competencies in-house and use external optimizers. The settlement structure then becomes a key issue – directly impacting the project’s risk profile and bankability.

Three basic cooperation models exist in the market: full merchant with profit share, tolling, and floor with revenue share.

Model 1: Full Merchant with Profit Share

In the full merchant model, the storage owner has no guaranteed minimum revenues. The optimizer manages the asset, generates market revenues, and parties share them according to an agreed split – typically 70-85% for the owner, 15-30% for the optimizer.

Model characteristics:

- Full exposure to market conditions – high revenues in good years, low in weak ones

- Aligned interests – the optimizer earns more when generating higher revenues for the owner

- Full transparency – the owner has visibility into actual market revenues

- Highest profit potential, but also highest risk

From a financing perspective, the full merchant model is hardest for banks to accept. No guaranteed minimum revenues means high cash flow uncertainty, requiring significantly higher equity contribution or additional security.

Market example: In October 2025, Axpo and Energix signed an agreement for optimization of a 24 MW / 56 MWh storage facility in Nowe Czarnowo (Axpo). The contract has a profit share structure with revenue split between parties.

Model 2: Tolling – Fixed Capacity Fee

In the tolling model, the optimizer pays the owner a fixed, predetermined fee for access to storage capacity. Regardless of market conditions, the owner receives a predictable revenue stream.

Model characteristics:

- Zero market risk exposure for the owner

- Predictable cash flows – ideal from a financing perspective

- The optimizer assumes all market risk and all potential upside

- Limited transparency – the owner doesn’t know how much the optimizer actually earns

Typical tolling rates are set at 50-70% of the storage’s theoretical revenue potential. The difference between theoretical potential and the toll rate represents the optimizer’s risk premium.

The tolling model is most preferred by financial institutions due to predictability. At the same time, the owner foregoes potential upside – if the market proves better than expected, the optimizer retains all the surplus.

Market example: In September 2025, Zelestra and BKW signed the first long-term tolling agreement in Italy for a project with up to 2 GWh capacity (Zelestra). This was the first such structure in the Italian market.

Model 3: Floor with Revenue Share – Hybrid Structure

The floor with revenue share model combines elements of both previous structures. The optimizer guarantees the owner minimum revenues (floor), and any surplus above this level is shared between parties.

Model characteristics:

- Limited market risk – the floor protects against worst-case scenarios

- Retained upside participation – the owner participates in revenue growth

- Higher optimizer fee (30-40%) – the price for minimum guarantee

- Full transparency – the owner sees actual revenues

The floor + revenue share structure represents a compromise between tolling safety and full merchant potential. From a financing perspective, it’s more acceptable than pure merchant, though it requires additional analysis of the floor guarantor’s creditworthiness.

Market example: In June 2025, EDPR and Axpo signed an agreement for optimization of a 60 MW / 241 MWh project in Greater Poland in a floor with revenue share structure (Axpo). The project also has a 17-year capacity market contract starting in 2029 – combining two stable revenue sources.

Model Comparison

| Criterion | Merchant / Profit Share | Floor + Revenue Share | Tolling |

| Owner’s market risk | Full | Limited | None |

| Profit potential | Highest | Medium | Lowest |

| Typical owner share | 70-85% | 60-70% + guarantee | Fixed fee (50-70% of potential) |

| Transparency | Full | Full | Limited |

| Bankability | Low | Medium | High |

| Optimizer motivation | Very high | High | Moderate |

Model selection depends on many factors: investor’s risk appetite, financing requirements, availability of other stable revenue sources (capacity market, PPA), and the optimizer’s financial condition as guarantor.

Largest Optimization Transactions in Poland

In September 2025, Greenvolt signed an agreement with Entrix for optimization of a 1.3 GW / 5.2 GWh portfolio – the largest such transaction in Poland (Greenvolt). Entrix, using AI-based algorithms, will manage optimization across all relevant energy markets, including FCR and aFRR balancing services and day-ahead and intraday markets.

According to Pexapark data (pexapark.com), Poland is becoming one of Europe’s most dynamic BESS markets. The opening of the ancillary services market in December 2024 resulted in revenues of EUR 208-305k/MW annually for utility-scale storage – significantly improving the sector’s investment attractiveness.

Technical Parameters Relevant to Optimization

Regardless of the chosen cooperation model, warranty documentation and storage technical parameters define the framework within which the optimizer can operate. These parameters directly impact revenue potential – and thus the achievable toll or floor level.

Key parameters:

- Cycle count – daily and annual cycle limits directly determine revenue potential. Storage with a 1.5 daily cycle limit will generate significantly lower revenues than an installation with a 2.5 cycle limit

- Resting period – required time between cycles for cell balancing limits operational flexibility

- Round Trip Efficiency (RTE) – guaranteed charge-discharge cycle efficiency affects the economics of every transaction

- C-rate and power limitations – charging power limits under specific conditions (temperature, state of charge) affect ability to respond to market signals

- BMS data quality – accuracy of battery management system readings is critical for optimization decision-making

A professional optimizer will require detailed technical documentation before submitting an offer. These parameters should also be included in the financial model presented to the bank.

Challenges Related to NFOŚiGW Subsidies

Subsidies from the National Fund for Environmental Protection and Water Management, while significantly reducing project CAPEX (up to 45% of eligible costs for large enterprises, 55% for medium, 65% for small), generate specific challenges in the bank financing process.

Priority in Security Structure

Subsidy agreements with NFOŚiGW typically contain provisions granting the fund priority in the project’s security structure. In case of enforcement – investor bankruptcy or project failure – NFOŚiGW has priority satisfaction before the financing bank.

From a financial institution’s perspective, this means significant deterioration of the lender’s position. In a typical project financing structure with a subsidy:

| Source | CAPEX Share |

| NFOŚiGW Subsidy | ~45% |

| Bank Loan | ~40% |

| Equity | ~15% |

In an enforcement scenario, if the project is sold for 50% of value, nearly all proceeds may go to NFOŚiGW (priority), leaving the bank with minimal recovery. This fundamentally changes the transaction’s risk profile from the lender’s perspective.

Time Pressure

An additional challenge is implementation deadlines arising from subsidy agreements. The project must be completed and settled within a specified timeframe – while bank negotiations proceed in parallel, which for BESS can be lengthy.

The market expects development of a standard tripartite agreement model (NFOŚiGW – Bank – Investor) that would resolve the priority issue in a manner acceptable to all parties – for example, through a pari passu structure (equal priority). According to market information, some subsidized projects have already closed bank financing, showing that solutions are possible – though they require more time and negotiation effort.

Regulatory Context: UC84

The UC84 draft law, adopted by the Council of Ministers in January 2026, introduces significant changes to grid connection rules for power installations. Key changes for BESS projects include:

- Shortening connection conditions validity from 2 years to 1 year – meaning a smaller time window for closing financing

- Doubling the advance payment for connection fees (from PLN 30 to 60/kW) – higher entry costs before obtaining financing

- Milestones in connection agreements – requirement to demonstrate building permit for 80% of capacity within 24 months

- Cable pooling extension to energy storage – a positive change enabling connection sharing

Detailed analysis of UC84’s impact on energy storage projects exceeds this article’s scope. However, it’s important that regulatory changes introduce additional uncertainty that must be factored into project timeline and budget.

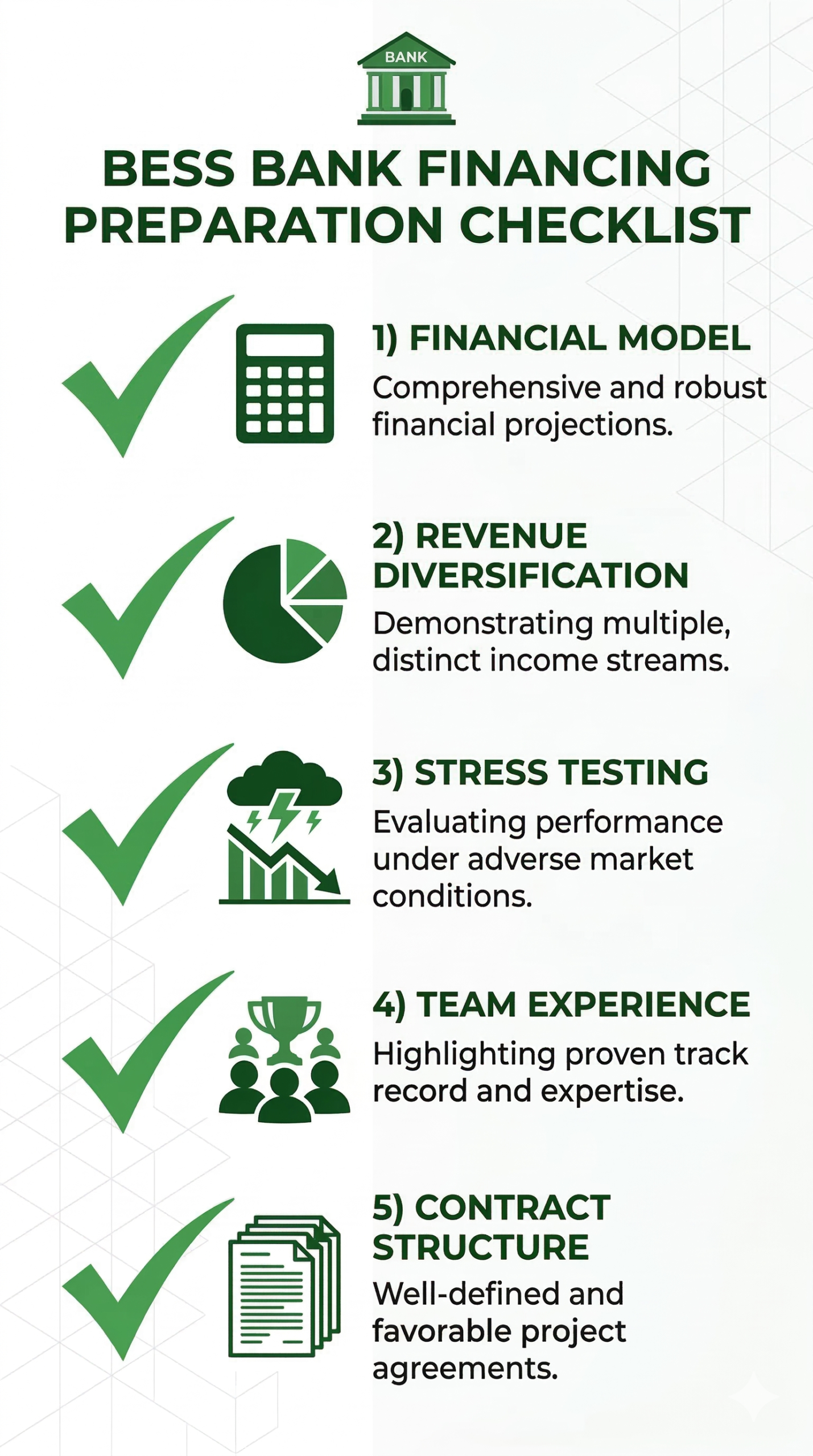

Preparing for Discussions with Financial Institutions

Successful BESS project financing requires proper documentation preparation and presentation of a credible business model. Below are key elements credit analysts focus on.

Diversified Revenue Profile

Projects based on a single revenue source are perceived as risky. The optimal structure combines multiple streams. The table below presents an indicative revenue breakdown observed in projects analyzed by GreenEdge:

| Revenue Source | Typical Share* | Characteristics |

| PPA / offtake contract | 40-60% | Highest predictability |

| Capacity market | 15-25% | Long-term, stable |

| Arbitrage (merchant) | 15-25% | Variable, spread-dependent |

| Ancillary services (FCR/aFRR) | 10-20% | Growing potential |

*GreenEdge estimates based on analysis of BESS projects in Poland and Europe. Actual structure depends on project specifics, contract terms, and optimizer strategy.

Scenario Analysis

The financial model should present at least three scenarios:

- Base case – most probable outcome, based on current forward prices and historical spreads

- Downside case – stress scenario (e.g., energy prices -30%, spreads -40%), showing the project’s ability to service debt under adverse conditions

- Upside case – optimistic scenario, illustrating project potential under favorable market development

Stress Testing

The bank will test project sensitivity to key variables:

- Faster battery degradation than warranted

- Lower RES curtailment (reduced arbitrage potential)

- No extension of optimization agreement after expiry

- Regulatory changes affecting ancillary services revenues

Track Record and Competencies

Financial institutions evaluate not only the project but also the sponsor and management team:

- Experience in energy project delivery

- Trading and optimization competencies (or credible external partner)

- Ability to operationally manage the installation

- Sponsor’s financial condition and ability to support the project if needed

Contractual Structure

Complete contractual documentation should include:

- EPC contract with performance guarantees and penalty schedule

- O&M agreement with guaranteed availability (minimum 95%)

- Optimization agreement with credible partner

- Construction, operational, and performance insurance

- Connection agreement with specified parameters

GreenEdge Solutions Support

GreenEdge Solutions offers comprehensive advisory services for BESS project financing:

Documentation Preparation for Financial Institutions

- Financial model development meeting bank requirements

- Price scenario and stress test preparation

- Technical documentation and due diligence

Commercial Structure Advisory

- Analysis of optimizer cooperation models

- Offer evaluation and negotiation support

- PPA and offtake agreement structuring

Regulatory Support

- Analysis of regulatory changes’ impact on project

- Connection process coordination

- Support in relations with NFOŚiGW

Summary

Financing BESS projects in Poland requires careful preparation and understanding of financial institutions’ perspective. While the energy storage market is developing dynamically, banks still treat this asset class with heightened caution.

Key conclusions:

- Project configuration is fundamental – hybrid projects (BESS + RES) are significantly easier to finance than stand-alone installations

- Capacity market remains the foundation – however, declining de-rating forces search for additional stable revenue sources

- Optimization model choice is a strategic decision – tolling maximizes bankability, profit share maximizes profit potential, floor + revenue share offers a compromise

- NFOŚiGW subsidies require additional work – priority issues in security structure complicate bank financing

- Documentation preparation is key – diversified revenue profile, scenarios, and stress tests build credibility with banks

- Early bank contact – starting discussions at development stage allows adapting project structure to financing requirements

The BESS financing market in Poland is professionalizing. Projects like EDPR-Axpo, Energix-Axpo, or Greenvolt-Entrix show that transactions are possible. Investors who properly prepare their projects – with appropriate commercial structure, documentation, and understanding of the bank’s perspective – will find financing, but it won’t be straightforward.

Sources

- Energy Storage News – Poland capacity market auction 2030: https://www.energy-storage.news/bess-wins-in-poland-capacity-market-falls-for-the-first-time-de-rating-cut-to-blame/

- Axpo – EDPR optimization agreement: https://www.axpo.com/group/en/news-and-stories/media-releases/2025/axpo-and-edp-sign-landmark-agreement-to-optimise-energy-storage-.html

- Axpo – Energix optimization agreement: https://www.axpo.com/group/en/news-and-stories/media-releases/2025/axpo-and-energix-join-forces-to-optimise-poland-s-first-utility-.html

- Greenvolt – Entrix partnership announcement: https://greenvolt.com/greenvolt-entrix-partnership/

- Zelestra – BKW tolling agreement Italy: https://zelestra.energy/zelestra-and-bkw-sign-innovative-long-term-tolling-agreement-enabling-the-delivery-of-a-major-2-gwh-battery-storage-project-in-italy

- Pexapark – BESS offtake deals in Poland: https://pexapark.com/blog/first-bess-offtake-deals-emerge-in-poland-as-market-gains-momentum/

- ESS News – NFOŚiGW subsidy allocation: https://www.ess-news.com/2025/12/19/poland-allocates-subsidies-to-14-5-gwh-of-energy-storage-projects/

- Norton Rose Fulbright – Cost of Capital 2024 Outlook: https://www.projectfinance.law/publications/2024/february/cost-of-capital-2024-outlook/

- NREL ATB – Financial Cases & Methods: https://atb.nrel.gov/electricity/2024/financial_cases_&_methods

Listen to the Podcast

More on BESS project financing in Episode 12 of the GreenEdge – Best in BESS podcast

Related articles:

BESS + PV: Why Hybrid Projects are the Future of Poland’s Renewable Energy Market

NIS2 and Cybersecurity in BESS Projects: New Obligations for Investors in Poland

Battery Energy Storage for Manufacturing: When Does BESS Make Sense for Industrial Facilities?