The Supplier Form and the Checkbox That Changes Everything

We increasingly encounter the same situation: an investor receives a BESS configuration form from a supplier — a few tables listing available system functionalities. Peak shaving, price arbitrage, FCR, aFRR, black start, grid-forming, island mode. The list is long and everything sounds appealing. The decision seems obvious: tick everything. But what for, exactly?

This is one of the most common mistakes made at the entry stage of a BESS project. Not because grid-forming is a bad technology — quite the contrary, it is increasingly important for system stability. The problem lies elsewhere: investors tick grid-forming on the form without any plan for how they will use that capability, what it involves technically, what it costs, or whether there is even a market product available to compensate for it.

This article explains what grid-forming actually is, what the regulatory landscape looks like across Europe and in Poland, and what you need to know before deciding whether this option makes sense for your project.

Grid-Forming vs Grid-Following: A Fundamental Difference

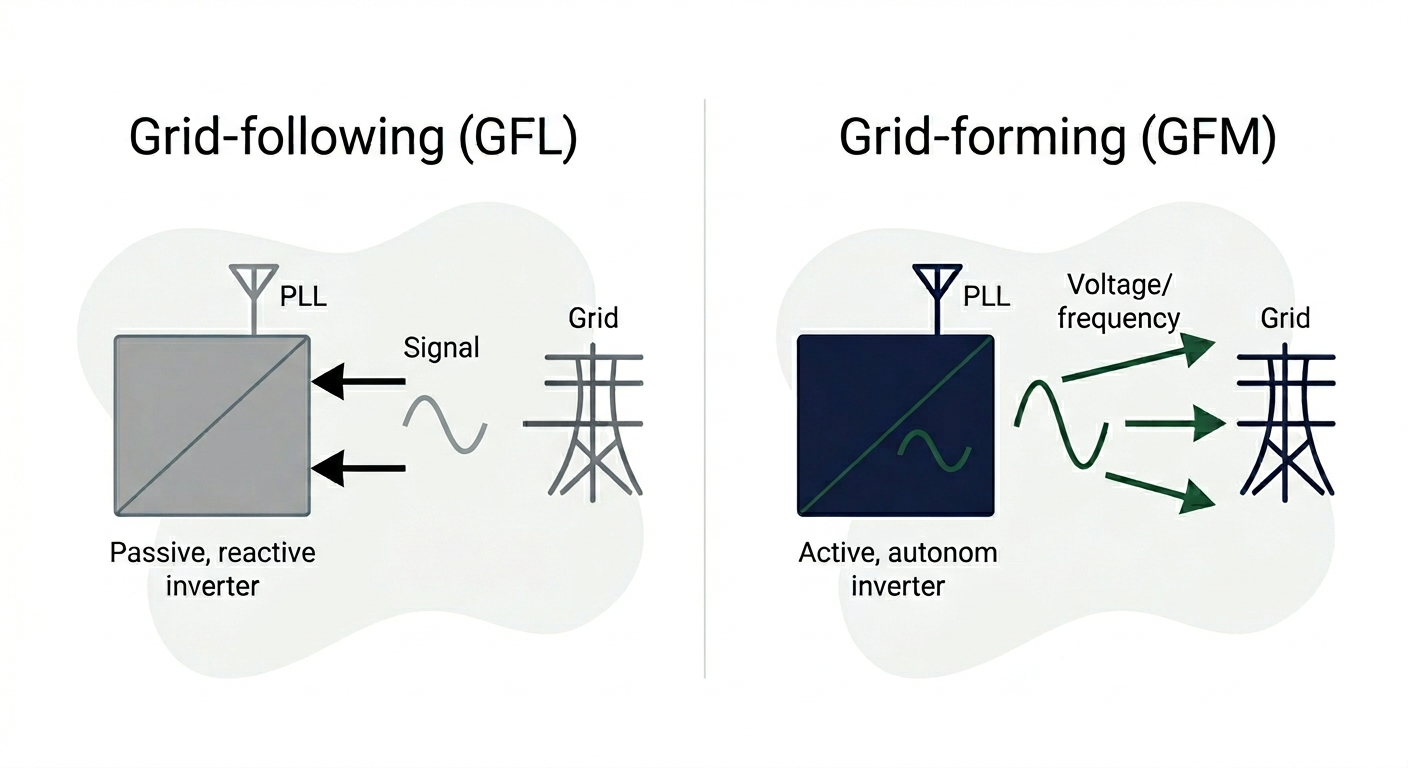

Most inverters operating in renewable energy and BESS projects today work in grid-following (GFL) mode. The inverter tracks the voltage and frequency of the existing grid using a Phase-Locked Loop (PLL) and synchronises its output accordingly. It functions as a perfect follower: the grid tells it what to do, and it complies. In a stable grid with a high share of synchronous generators, this approach has proven entirely adequate for decades.

The problem arises when the grid weakens. As coal and gas power plants exit the system, they take with them something a GFL inverter cannot replace: inertia. The rotating masses of generator turbines act as enormous flywheels — they slow down frequency changes following disturbances and give the system time to respond. A GFL inverter generates no inertia: it reacts to grid frequency, but does not stabilise it.

A grid-forming inverter (GFM) works in reverse. Rather than tracking the grid signal, it creates its own voltage and frequency at the point of connection — operating programmatically, it behaves like a synchronous generator. It can function even when the grid is entirely dead (black start). It can respond to disturbances within milliseconds, without waiting for a signal from the network operator. It can maintain voltage at weak grid nodes.

This sounds like a solution to everything. And that is precisely where the problem with that checkbox begins.

28 April 2025: The Iberian Blackout and What It Actually Tells Us

On the 28th April 2025, at 12:33 CET, a major power outage struck the Iberian Peninsula — Spain, Portugal, Andorra, and parts of southern France. More than 50 million people were left without electricity for several hours. In the weeks that followed, media coverage offered a simple explanation: too much solar and wind, too little inertia.

The ENTSO-E final report published in March 2026 dismantled that narrative. The blackout was not caused by the share of renewables per se — it was the result of a combination of overlapping factors: voltage oscillations, gaps in reactive power control, differences in voltage regulation practices between regions, sudden generation reductions, and cascading generator trips. It was primarily a voltage control failure, not simply an inertia deficit.

Why does this matter? Because a significant volume of conference materials and BESS supplier sales collateral published since May 2025 cites the blackout as evidence for the necessity of grid-forming technology. That is an incomplete narrative. Grid-forming is one of ENTSO-E’s recommendations following the event — but it is neither the sole nor the primary diagnosis. An investor who understands this distinction will be better placed to evaluate aggressive marketing.

What the Iberian blackout legitimately demonstrates is this: in a system with a growing share of renewables and retiring synchronous generators, grid stability becomes a structural challenge. Poland will be in a similar position in a few years to where Spain was several years ago. That is an argument for understanding the topic more deeply — not for alarm.

How Europe Is Addressing the Inertia Problem: Three Models

Each country is taking its own path, but the direction is consistent.

United Kingdom: The Pioneer That Proved It Works — and Revealed the Pitfalls

The UK was the first country in the world to define grid-forming requirements in a grid code. Specification GC0137 (GB Grid Forming Capability) received regulatory approval in 2022. National Grid subsequently launched the Stability Pathfinder programme, procuring inertia and short-circuit level services from private assets.

Under Stability Pathfinder Phase 2, NESO awarded a total of 10 contracts worth £323 million, securing 11.55 GVA of short-circuit level in Scotland and 6.75 GVA·s of inertia for Great Britain — delivered through five synchronous condensers and five grid-forming batteries.

The flagship operational example: Zenobē, with Wärtsilä (BESS systems and GEMS platform) and SMA Solar (grid-forming inverters), brought Blackhillock in Scotland online — the first battery in the world to deliver Stability Services directly to a transmission system operator. The commercial model was built on revenue stacking: stability services were combined with day-ahead trading, frequency reserves, reactive power, and balancing — allowing the operator to receive services at a fraction of the cost of a purely stability-focused project.

There is, however, a second side to this story. In Stability Market Round 2, conducted in early 2026, NESO awarded no contracts to BESS projects — every battery submission failed at the technical assessment stage. Contracts totalling 7.3 GVA went to synchronous condensers and open-cycle gas turbines (OCGTs). Industry participants suggest the procurement’s technical specifications — requiring bidders to commit to fixed, non-variable inertia constant values — may have been better suited to synchronous technologies than to the characteristics of BESS. The grid-forming technology performed in the Pathfinder. In the subsequent tender, it did not pass the formal compliance requirements. This is the essential lesson about the difference between “grid-forming capable”, “grid-forming certified”, and “grid-forming compliant with a specific procurement”.

Germany: The First Revenue Product, Live Since January 2026

Germany has gone furthest in establishing a commercial compensation mechanism for grid-forming capability.

In May 2025, the VDE FNN guideline on grid-forming requirements and verification entered into force — Germany’s first such standard. On that basis, and following a Bundesnetzagentur decision in April 2025, Germany’s four transmission system operators — 50Hertz, Amprion, TenneT, and TransnetBW — launched inertia procurement under the name Momentanreserve on 22 January 2026.

The model: a fixed payment per registered MW, with four product categories differentiated by direction of inertial response and availability level. The premium product (90% availability) is designed for BESS — higher compensation in exchange for higher operational readiness. Contracts run for two years from commissioning, with TSO acceptance within three months of submission.

Entry requirement: compliance with VDE FNN technical specifications — a supplier’s “grid-forming capable” declaration is not sufficient.

This is the model Poland should be watching as a reference point for a future PSE product.

Ireland: A 95% SNSP Target by 2030 and a Pragmatic Pilot

EirGrid has set a target of 95% non-synchronous penetration (SNSP) by 2030. Reaching that level requires synchronous condensers, grid-forming inverters, and advanced frequency management. Under the Low Carbon Inertia Services (LCIS) programme, inertia has already been contracted from four projects.

The LCIS Phase 2 document from December 2025 is nonetheless notably cautious: grid-forming does not meet the qualification requirements for the main inertia procurement — primarily because BESS does not deliver short-circuit level to the same extent as synchronous condensers. At the same time, EirGrid has announced a separate pilot for grid-forming technology. The approach of “we want this, but we need to formally validate it first” is both honest and worth watching from a Polish perspective.

ENTSO-E and NC RfG 2.0: Direction Certain, Timeline Uncertain

ENTSO-E has published its Phase II Technical Report on grid-forming requirements — the foundation for a future mandatory grid-forming obligation for large-scale renewables and BESS installations above 1 MW. The report is non-binding, but the framework is effectively final.

A critical detail that tends to disappear in marketing materials: NC RfG 2.0 is still working through the European Commission’s legislative process and has no confirmed adoption timeline — resumption of work is planned for 2026, but no adoption date exists. Once adopted by the Commission, each EU member state will implement the requirements according to its own approach and timetable, potentially with transitional periods. The full path for Poland — from NC RfG 2.0 adoption through transposition into IRiESP and eventual market products — is a multi-year process with deep uncertainty at every stage.

The Regulatory Situation in Poland: June 2026

This is the section requiring the greatest precision, because the market is full of misleading signals.

Where Things Stand Today

PSE is present at conferences and speaks about grid-forming. The PSE Strategy 2026–2040, published in December 2025, lists grid-forming as one of the pillars of grid stability — alongside synchronous compensators and the development of ancillary services markets. PSE has also announced the publication of an “Electricity Market Roadmap” in 2026, which will identify new product requirements. This may be the first signal of PSE’s approach to compensating grid-forming capability — but as of today, it remains an announcement.

Key excerpt from the PSE communication of January 2026: “As coal-fired power plants are phased out, synchronous generators will also disappear from the National Power System. These generators provide, through their physical characteristics, properties critical to grid operation — such as inertia, short-circuit power, and voltage regulation capability. To date, renewable energy sources have been unable to provide these, as the vast majority operate in grid-following mode.”

What Is Planned

PSE is currently conducting market reconnaissance and technical dialogues with GFM technology suppliers — identifying available solutions and assessing their technological maturity. PSE is also reviewing the experience of other European TSOs.

The second stage — drafting technical requirements and conducting industry consultations — is planned for the second half of 2026. PSE explicitly states: the scope, timeline, and form of implementation may change depending on the outcomes of its analyses and regulatory conditions.

What Does Not Exist and Will Not Exist in the Near Term

As of June 2026:

There is no binding technical grid-forming standard in IRiESP or any regulation. There is no PSE market product compensating grid-forming capability (no equivalent of Momentanreserve or Stability Pathfinder). There is no grid-forming certification process in Poland. There is no defined pathway for demonstrating this capability at the point of connection. There are no clear answers to the question: what happens to a project that has declared grid-forming capability but has no certificate — because there is nothing yet to certify against.

Why Investors Tick “Grid-Forming” Without a Plan

Let us return to the form.

First, the psychology of optionality. The investor thinks: I’ll tick it now, I have nothing to lose, and maybe in a few years I’ll be able to use it. This is an understandable instinct. The problem is that grid-forming is not a switch. It is an architectural decision made at the PCS design stage, with consequences for the technical specification, verification and certification costs, the operational model, and — critically for bankability — the scope of EPC warranties.

Second, supplier pressure. “Grid-forming capable” justifies a higher CAPEX figure and looks better in marketing materials. The supplier is happy to tick the box — but responsibility for the revenue plan rests with the investor.

Third, the absence of the right question. No one comes to the investor and asks: what is your revenue plan for this capability? Where is the contract? Which PSE product will pay for it, and when? These are the questions that should be raised at the due diligence stage — before the EPC contract is signed.

Checklist: What to Actually Verify in a Supplier Offer

When you see “grid-forming” in a BESS technical specification, these are the right questions to ask:

- What exactly does “grid-forming capable” mean in this offer? Does the inverter hold certification against a specific standard (VDE FNN, GC0137 GB)? Is this a firmware feature that can be activated without hardware replacement? Does it require additional components? Does the manufacturer provide EMT (Electromagnetic Transient) models required for GFM capability verification by the network operator? Without EMT models there is no certification — what does this cost and how long does it take?

- Who verifies this capability and through what process? In the UK, grid-forming verification requires specialist simulation testing and compliance protocols that go beyond the standard grid connection process. In Poland as of June 2026, no such process exists. What does this mean for your project in the event of a material modification to the installation once NC RfG 2.0 is in force?

- What is the revenue plan for this capability? In Poland today there is no PSE market product compensating grid-forming. If a supplier or developer says “there will be earning opportunities” — ask: from what specifically, on what timeline, and on the basis of which regulatory document?

- Is grid-forming consistent with the operational model? Grid-forming — particularly when providing synthetic inertia — requires maintaining SOC within a specific readiness band. This affects the availability of capacity for other services and the relationship with the aggregator or optimiser. Does your operational model account for this ongoing cost?

- Is a retrofit possible if you decide to wait? In some cases, upgrading to grid-forming is achievable through a firmware update without hardware replacement — Australia’s Western Downs Battery (540 MW / 1,080 MWh) followed this path in 2025. However, not every inverter supports grid-forming control at the firmware level. Ask your supplier directly: is this option available for my specific PCS, and what does it cost and how long does it take?

When Grid-Forming Actually Makes Sense

Grid-forming is a real and important technology. The decision to include it should, however, be based on a concrete rationale — not on the reflex of ticking everything available.

C&I Installations with a Genuine Operational Requirement

This is today the most justified use case in Poland. An industrial client has a specific reason for needing supply that is independent of the grid: a mine that must evacuate workers during a power failure. A production line that must safely return machinery to its starting position. A data centre with contractual continuity-of-supply obligations.

But here is the part that BESS suppliers often do not communicate clearly. The “grid-forming” checkbox on the form is only the starting point. For island mode to actually function, the following are required:

- design and installation of dedicated electrical infrastructure enabling network separation (appropriate busbars, switchgear, transfer switching arrangements),

- an automatic protection system capable of detecting grid loss within milliseconds and safely transferring the installation to island mode — without loss of supply or equipment damage,

- coordination with the distribution network operator, who must be aware that the installation can operate in island mode and must accept this in the connection agreement,

- a protection coordination study to ensure the island arrangement does not conflict with the DSO’s own protection automation,

- commissioning documentation and acceptance testing confirming that the entire chain functions as an integrated system, not as a collection of individual components.

In short: grid-forming as a PCS function is one piece of the puzzle. An island-mode project is a separate engineering scope that must be planned from the outset — not appended as a post-contract variation to the EPC.

Building Optionality for Future Revenue Streams

The second justified case: an investor consciously designs the system with a future PSE market product in mind, or in anticipation of NC RfG 2.0 requirements reaching Polish law.

But honesty is required about what you are actually deciding. Today, the following remain unknown: what technical parameters PSE will set in its GFM requirements; what the certification process will look like — because no guidelines exist yet; what the network operator will require at the point of connection or upon material modification of the installation; and what timeline a market product will emerge on and how it will be priced.

Ticking “grid-forming capable” in the BESS supply contract resolves none of these questions. It gives you an inverter with the appropriate firmware — but not a certificate, not the EMT models required by the operator, and not readiness for a procurement whose requirements do not yet exist.

If you are building optionality, do so consciously: with an analysis of exactly what you are buying today, what remains to be resolved later, and what the realistic regulatory scenarios are. This is a legitimate investment decision. But it should be made with eyes open — not with the sense that ticking the checkbox has closed the matter.

What PSE and the Market Will Do Next: An Honest Forecast

In the second half of 2026, PSE’s draft GFM technical requirements and limited industry consultation should emerge. This will be the moment the market sees concrete parameters and can assess which installations currently under construction or in planning will need to meet new requirements in the event of a material modification, in line with NC RfG 2.0.

In the same year, PSE has committed to publishing an “Electricity Market Roadmap” — a document identifying new product requirements. If it contains any reference to compensation for grid-forming or synthetic inertia, this will be a significant signal for investors building revenue models on a 10-year-plus horizon.

NC RfG 2.0 adoption at EU level is planned for 2026, but with an uncertain timeline. Once adopted by the European Commission, each country will implement requirements at its own pace, with potential transitional periods. The full path for Poland is a multi-year process.

A PSE market product compensating grid-forming will be possible within a few years, but without any official announcement of parameters or timeline. Anyone who says otherwise is selling a forecast as a fact.

Summary: What to Tick and What to Question

Grid-forming is transitioning from a technical curiosity to a structural element of stability in systems dominated by renewables. Germany has launched a market product. The UK has demonstrated that the technology works — and simultaneously shown that “capable” is not the same as “certified” and “compliant with a specific procurement”. Ireland is piloting cautiously. ENTSO-E is finalising a legal framework whose adoption is a matter of years, not months.

In Poland, PSE is at the market reconnaissance stage. No standard, no certification pathway, and no market product yet exist.

A supplier form offering “grid-forming” is not a revenue proposal. It is an architectural decision with financial, technical, and operational consequences — one worth making deliberately.

Three questions worth considering before ticking the checkbox:

- Which standard? — VDE FNN, GC0137, or a supplier declaration only?

- What revenue? — Which market product, on what timeline, based on which regulatory document?

- What cost? — CAPEX, EMT verification, certification, impact on the operational model?

If you do not have answers to these three questions — the checkbox can wait.

How GreenEdge Can Help

Grid-forming is appearing in BESS projects earlier and earlier — often already at the supplier selection and EPC negotiation stage. We support investors at each of these stages.

BESS supplier offer assessment

We verify what actually sits behind a “grid-forming capable” declaration in a specific offer: which standard, which firmware, what certification requirements, and what the consequences are for EPC scope and warranties. We separate marketing language from technical commitment.

Technical Due Diligence for BESS projects

If you are acquiring an RTB project or assessing it as a financial investor, we verify whether the PCS specification is consistent with the declared functionalities — including grid-forming, black start, and island mode. We identify gaps between the form and the technical reality.

Regulatory advisory

We track the PSE process (GFM technical requirements, Electricity Market Roadmap) and NC RfG 2.0 developments at EU level on an ongoing basis. For projects with a 10-year-plus horizon, we help assess regulatory risk and build a substantiated revenue scenario — without selling forecasts as facts.

EPC specification support

We prepare tender documents and technical specifications that clearly define the grid-forming scope: what is included in the contract, what is optional, what the verification requirements are, and what contractual penalties apply in the event of non-compliance.

If your project already has grid-forming on the supplier form — contact us before signing the EPC contract: contact@greenedge-solutions.com

Sources

- ENTSO-E, Phase II Technical Report on Grid Forming Requirements, November 2025 — entsoe.eu

- ENTSO-E, Final Report on the 28 April 2025 Blackout in Spain and Portugal, March 2026 — entsoe.eu

- ENTSO-E, 38th Grid Connection European Stakeholder Committee — Minutes, 2025 — eepublicdownloads.blob.core.windows.net

- VDE FNN, Guideline Grid-Forming Capabilities, May 2025 — vde.com

- NESO, GC0137 — Minimum Specification Required for Provision of GB Grid Forming Capability, 2022 — neso.energy

- Herbert Smith Freehills Kramer, Germany to Launch Inertia Service Market in 2026, October 2025 — hsfkramer.com

- Energy-Storage.News, Germany’s TSOs Begin Inertia Procurement with Long-Term Contracts for Grid-Forming BESS, January 2026 — energy-storage.news

- NESO, Great Britain’s First Grid Forming Battery Connects in Scotland, March 2025 — neso.energy

- Solar Power Portal / Modo Energy, NESO Gives No Contracts to Batteries in Stability Market Round 2, March 2026 — solarpowerportal.co.uk

- EirGrid/SONI, LCIS Phase 2 Arrangements Recommendations Paper, December 2025 — eirgrid.ie

- EirGrid/SONI, Operational Policy Roadmap 2025–2035, March 2025 — eirgrid.ie

- PSE, Guardian and Architect — PSE Strategy to 2040, December 2025 — pse.pl

- PSE, PSE Begins Work on Grid Parameter Shaping by Energy Storage Systems, January 2026 — pse.pl

- Gramwzielone.pl, Energy Storage Systems Will Shape Grid Parameters. PSE Developing Specific Requirements, January 2026 — gramwzielone.pl

- Intersolar/Rogalla, Standardization of Grid-Forming Inverters in the EU, November 2025 — intersolar.de

- Enertis Applus+, Grid-Forming Inverters: Technical and Economic Insights, April 2026 — enertisapplus.com

- Modo Energy, Grid-Forming: From Niche Upgrade to Standard Requirement, April 2026 — modoenergy.com

- ScienceDirect, Review of Recent Developments in Grid Codes: Focus on Compliance Testing and Grid-Forming Inverter-Based Resources, November 2025 — sciencedirect.com

Article prepared by GreenEdge Solutions on the basis of regulatory documents and industry materials on grid-forming technology and ancillary services markets in Europe. Regulatory status: June 2026. This article is for informational purposes only and does not constitute technical or investment advice.

Listen to the podcast:

Related articles:

UC84: Grid Connection Revolution — Part 2. Retroactivity and other changes

UC84: New Grid Connection Rules for BESS and Renewables in Poland

Financing Energy Storage in Poland: How to Finance a BESS Project in 2026